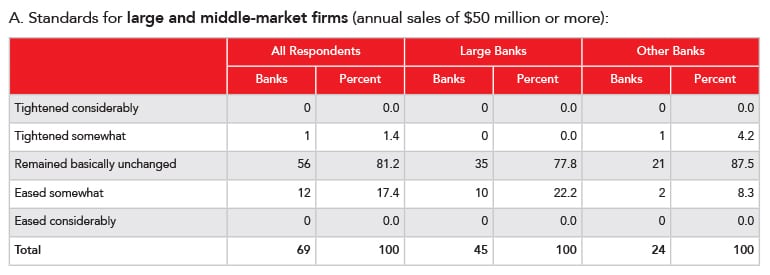

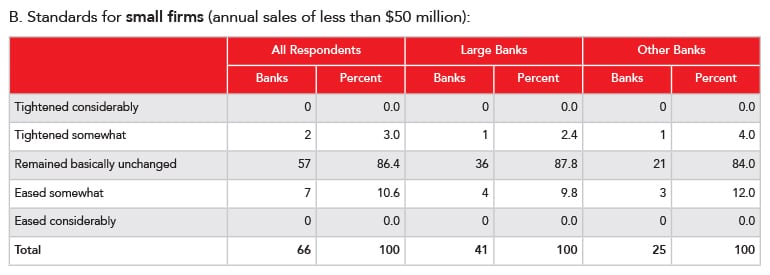

U.S. banks eased their terms and standards for commercial and industrial loans in the second quarter, according to a July survey by the U.S. Federal Reserve.

However, they kept commercial real estate and construction and land development lending standards about the same, according to the July 2018 Senior Loan Officer Opinion Survey on Bank Lending Practices.

Demand was stronger for C&I loans among small firms, but weaker for CRE loans. It was about the same for construction and land development loans.

Most banks that eased their standards on C&I loans pointed to heightened competition from other lenders as the reason, according to the Fed. They also noted a more favorable economic outlook, increased risk tolerance and increased liquidity in the secondary market as factors.

“The basic takeaway is very competitive conditions, especially for higher quality C&I credit,” said Bryce Rowe, senior equity research analyst covering community banks at Milwaukee-based Robert W. Baird & Co. Inc. “Since the financial crisis, C&I has been the primary focus of banks and it’s what you hear a lot of the community bankers focusing on in terms of where they want their growth and where they want their loan growth.”

Wisconsin banks have generally been matching those national trends, said Rose Oswald Poels, president and chief executive officer of the Wisconsin Bankers Association.

U.S. banks’ Q2 credit standards for C&I loans

“I know there is growing competition in the C&I lending space from all institutions, so rates and terms are getting a little bit better,” Oswald Poels said. “That doesn’t necessarily mean if you don’t meet their underwriting criteria that you’re going to get a loan.”

That competition means the terms are getting more favorable for borrowers, so it could be a good time for businesses to consider seeking a C&I loan, she said.

“2018 continues to be a very positive environment for businesses in terms of borrowing money,” she said. “I think they’ll find lots of good options in terms of loan terms and pricing. If a business is looking to borrow money, now is the time to do it before rates continue to slowly climb.”

Since the Fed is gradually raising interest rates, some banks have started to pay more attention to shoring up their funding reserves, Rowe said.

“With incremental interest rate hikes by the Fed, the focus has kind of shifted to how to fund loans,” he said. “The incremental funding cost has gone up, so banks that might have a higher loan-to-deposit ratio or are needing funding to fund that extra loan, they might be a little more sensitive to pricing.”

Loosened standards come across in better loan pricing, covenants and structures, terms, and extended maturity, Rowe said.

Banks’ loosened C&I terms are a little bit riskier, but there is still a lot of pressure on commercial real estate loans from a regulatory perspective as a result of the financial crisis, he said.

“Banks have been cautioned to remain at a certain level of commercial real estate to capital,” Rowe said. “Smaller commercial banks, they’ve done more commercial real estate lending than you would see from the larger banks, at least as a percentage of their loan portfolios.”

As for when banks’ standards and terms could tighten back up, Oswald Poels said the lending environment will follow the current economic cycle.

“What causes banks to make changes to loan terms that are more negative from the standpoint of a borrower really ties in to the health of the borrower themselves,” she said.

After the financial crisis of 2008, the federal government put in place more regulations and oversight, so Oswald Poels does not expect banks to get back into the realm of irresponsible lending, she said.

“I don’t think that the industry is offering loan terms that are what I guess you could call silly loan terms, the type that are going to get the bank in trouble,” Oswald Poels said. “I don’t see the pendulum moving back that far at all.”

Being in a late-stage economic growth cycle, it’s tough to say whether the pendulum has swung too far, Rowe said. But it wouldn’t be on CRE loans.

“I think most folks would agree that you’ve seen corporate debt levels explode higher and that’s where the primary risk is these days,” driven by widespread stock buybacks, he said.

Jay Risch, secretary of the Wisconsin Department of Financial Institutions, said Wisconsin’s economy is doing well and its banks and borrowers are generally more conservative in their lending practices.

“Our examiners are looking at the whole picture of a bank’s lending practices,” Risch said. “The good news is as a whole…they’re doing things right to remain safe and sound and still be offering those loans that help fuel the economy.”