Several Wisconsin-based insurance providers are restructuring their companies to remain competitive as innovative technologies bring new opportunities and disruption to the industry.

In recent years, a growing number of insurance companies either have reorganized or are in the process of reorganizing from mutual insurance companies into mutual holding companies — a change that offers them more flexibility to engage in acquisitions, raise capital, and diversify their products and services.

Madison-based American Family Insurance is credited with kicking off the trend in 2016 when its policyholders approved its conversion from a mutual insurance company to a mutual holding company. Under the structure change, American Family Mutual Insurance Company, the original entity, became a stock subsidiary company wholly owned by the newly created mutual holding company.

Company leaders at the time said the new structure would pave the way for American Family to invest in or acquire non-insurance companies that specialize in protecting customers, such as smart-home technology and distracted-driving prevention, and to acquire other mutual insurance companies.

Since then, four other Wisconsin insurance companies have followed suit by restructuring or beginning the process, including Church Mutual Insurance, Jewelers Mutual Insurance, Sentry Insurance and SECURA Insurance.

Experts say this corporate restructuring trend reflects efforts by some insurance companies to get out ahead of industry disruptors, including new technologies, like autonomous cars, that will likely lower premium volumes. Without restructuring, some of Wisconsin’s insurance companies could fall behind the competition, insurance leaders say.

Merrill-based Church Mutual considered various options – including remaining a mutual insurance company or demutualization — before ultimately deciding to convert to an MHC.

“The insurance industry, we’ve been pushed,” said Mike Smith, Church Mutual senior vice president, secretary and chief legal counsel. “And this is a way within the regulatory framework that we can be responsive. The MHC puts us on a level playing field and allows us to invest in … other technologies as they present themselves.”

The option to restructure as a mutual holding company was first made available under Wisconsin law in 1997 to address certain disadvantages of the mutual insurance company structure. Under that structure, insurers can’t raise capital through the sale of stock, acquire another mutual insurance company without ending the legal identity of the acquired company, or hold significant assets in non-insurance subsidiaries. The change in state law addressed some of those competitive disadvantages by allowing the mutual insurance companies to covert into a stock company while still preserving the company’s mutuality, or policyholder ownership.

While new innovations in home security, fire prevention or safe-driving applications are expected to potentially lower premiums, converting to an MHC gives insurers more flexibility to pursue a stake in those technologies.

“The expectation in the property-casualty industry is that claims will go down and that insurance companies that want to grow, succeed and compete in the future are considering investments in these synergistic technologies,” said Anne Ross, an attorney with Foley & Lardner who specializes in corporate restructuring.

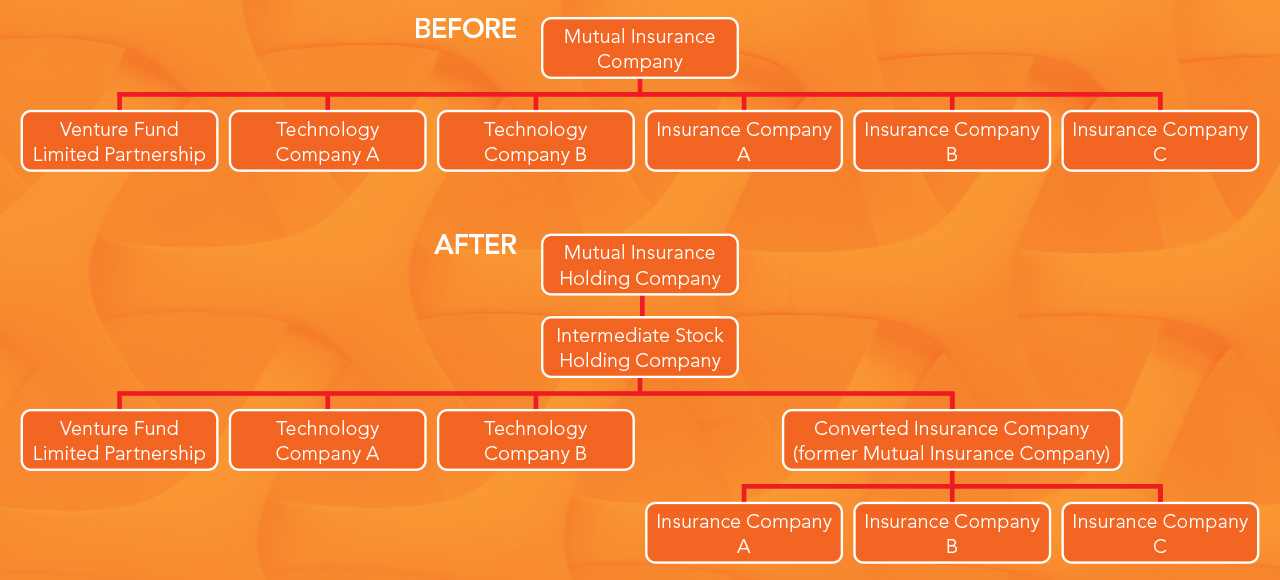

The MHC structure enables a company to move its technology-oriented subsidiaries out from under the insurance company parent so that they are owned directly by the mutual holding company or an intermediate stock holding company. The company is then able to grow and retain any earnings generated by its non-insurance businesses.

“These are no longer assets that the company is relying on to pay claims,” Ross said. “They are no longer counted as part of the policy holder surplus that is the key measure of the financial strength of the insurance company and its ability to pay claims.”

Smith likens the disruptive effect of technology on the insurance industry to how Uber and Lyft shook up the taxi industry.

“If you think about what happened to taxis with Lyft and Uber, that technology forced the taxi industry and the regulation around it to revaluate itself, and look where we are today,” Smith said.

However, Ross noted insurance companies haven’t yet seen premium volumes drop significantly because of new technologies.

“You’re not really seeing the full impact on revenue yet,” Ross said. “This is more forward-looking.”

Meanwhile, some say the MHC trend could be good news for Wisconsin’s venture capital ecosystem, which, despite some growth in recent years, continues to lag its Midwestern neighbors.

Tom Hefty, retired chief executive officer of Blue Cross-Blue Shield of Wisconsin and former deputy commissioner of insurance for Wisconsin, said it will increase the pool of venture capital available in the state while attracting more outside investors to Wisconsin.

“Wisconsin Technology Council has long published papers on the shortage of venture capital in Wisconsin,” said Hefty, a former council board member. “One of the reasons that Wisconsin did not have much venture capital over the last 20 years was the fact that the insurance industry in Wisconsin could not participate in venture capital deals.”

For many insurance companies, including Church Mutual, maintaining mutuality is just as important as the additional leeway to invest in technologies. In an MHC, the insurance company owners are also customers, compared to a publicly traded company in which shareholders may or may not have a policy with the company.

“For us as employees working for an MHC, we still understand that we work for the policyholders,” Smith said. “That’s a very different environment than, say, working for a publicly traded insurance company where shareholders own the company.”

Several Wisconsin companies that have made the change cited the ability to expand mutuality as a benefit of restructuring. Through the conversion, policyholders of an affiliated stock insurance company, which are often formed by mutual insurance companies to sell new product lines, can become members of the MHC along with the policyholders of the converted mutual insurance company.

Restructuring requires approval from policyholders, the company’s board of directors and from the Wisconsin Office of the Commissioner of Insurance. OCI is tasked with ensuring that an insurer has adequate funds earmarked to pay claims and that funds aren’t distributed to shareholders in excess or placed in risky investments.

Insurance company organizational chart

The insurance company organizational chart represents the typical structures of mutual insurance companies and mutual holding companies and their differences, although each structure can be significantly more complex. Courtesy of Anne Ross, attorney at Foley & Lardner.

Anne Ross[/caption]

Anne Ross[/caption]